TL;DR: 1.15 million Canadian homeowners renewing mortgages in 2026 focus on lowering monthly payments. Wrong move. You should focus on total interest paid. Extending a $400,000 mortgage from 15 to 25 years? You’ll pay an extra $100,000 in interest. Automatic renewal? You’re throwing away $9,300 over five years. Principal acceleration matters more than payment comfort.

The Numbers You Need:

-

Extending amortization wipes out $100,000 in equity over the loan lifecycle

-

69% of Canadians auto-renew and pay $155 more monthly ($9,300 over five years)

-

Accelerated bi-weekly payments and lump sums cut amortization by 2 to 3 years

-

Keep 3 to 6 months of expenses liquid before making extra payments

-

Treating renewal as ongoing rebalancing beats one-and-done decisions

The Biggest Mortgage Renewal Mistake in 2026

Data shows a clear pattern.

1.15 million Canadian homeowners are solving for lower monthly payments when they should solve for total cost.

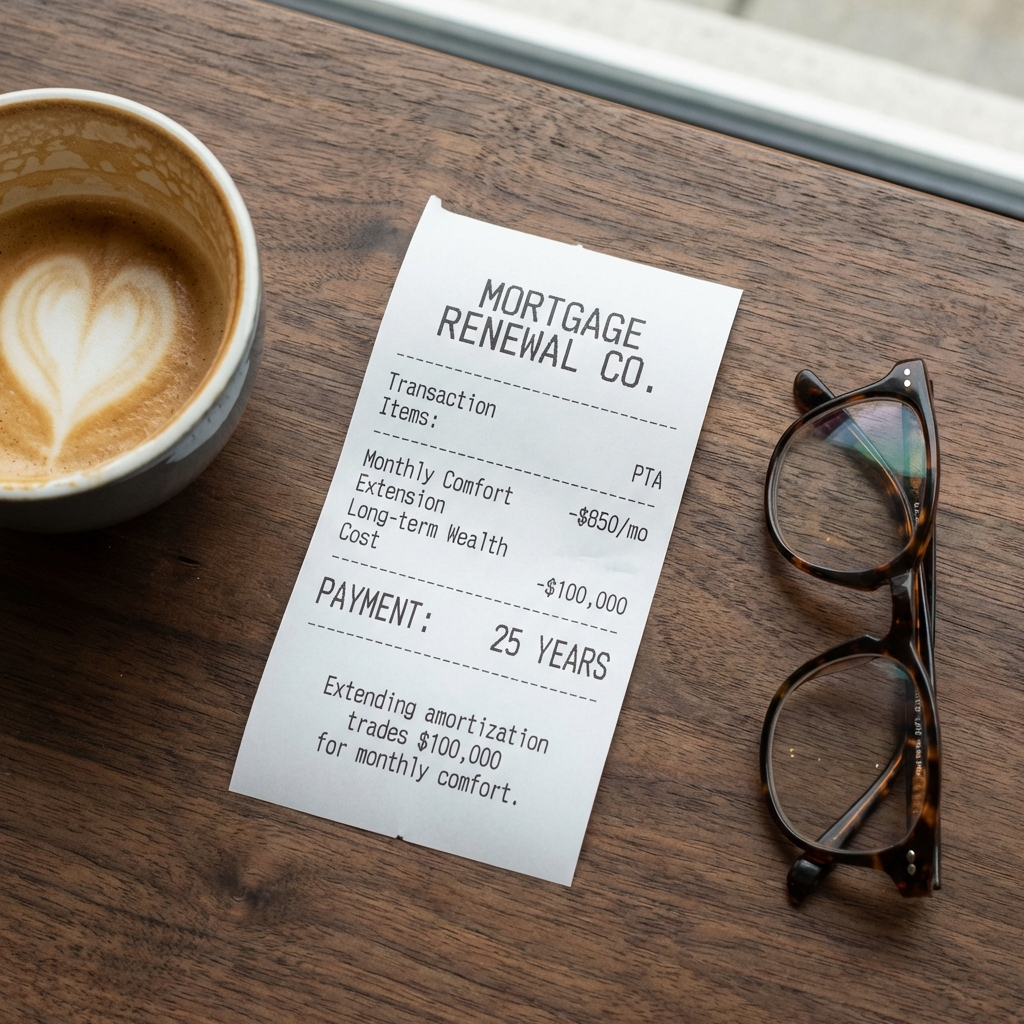

Here’s what happens. On a $400,000 mortgage at 4%, extending from 15 years to 25 years drops your monthly payment by $850.

But total interest jumps from $132,000 over 15 years to $233,000 over 25 years.

An extra $100,000 in interest costs.

Most borrowers see the monthly relief. They sign the letter. They miss the $100,000 difference.

The $15 billion annual increase in mortgage payments across Canada? Not the real crisis.

The crisis is people solving for the wrong thing.

Bottom Line: Lower monthly payments feel good now. Lower total interest builds wealth over time.

How Auto-Renewal Costs You $9,300

The biggest mistake homeowners make? Accepting the first offer from their lender.

Lenders send a sign and confirm letter.

Lenders make signing easy.

69% of Canadians stick with their lender at renewal.

People who auto-renew pay $155 more per month versus those who shop around.

Over a five-year period, $9,300.

Not a small error.

You’re transferring wealth from yourself to the bank because switching feels hard.

Lenders know how people behave. Auto-renewal locks you into shorter terms with higher rates. You give up negotiating power.

Auto-renewal costs you 15 to 25 basis points.

Bottom Line: Doing nothing costs $9,300 over five years. Shopping around isn’t optional.

Why Most People Solve for the Wrong Thing

Homeowners focus on monthly payment cuts.

They should focus on total cost.

Lenders focus on monthly affordability. They don’t show you what higher rates cost over decades. Your renewal letter? No mention of total interest.

Most borrowers don’t see the $100,000 gap when they sign.

They see monthly relief. Problem solved, right? Wrong.

The opportunity cost calculation is significant.

Take $4,000 per year (the $100,000 spread divided by 25 years). Invest it annually at 8% for 25 years. You’d have $292,418.

Extending amortization means paying $100,000 extra instead of cutting spending now.

Math doesn’t lie.

If you can’t find $6,500 in annual savings, you have an income problem, not a mortgage problem.

Extending to 25 years isn’t solving anything. You’re delaying the problem and paying extra for the delay.

An advisor who suggests extending without showing total interest? They’re making you comfortable, not wealthy.

Bottom Line: The $100,000 gap destroys your equity growth and wipes out investment gains. Lenders hide this because showing you hurts their profits.

How Business Failure Changed How I See Debt

I used to think managing debt was secondary.

At 47, I lost almost everything when my business failed.

Failure changes how you see money.

Paying interest became priority one. Over 10 years, I’ve paid zero in credit card or line of credit interest.

Now I borrow only when returns beat interest costs by a specific margin.

Mortgages work on big numbers. Rates look low compared to credit cards, but small rate changes hit hard over 5, 10, or 15 years.

This compounds total cost of ownership.

Bottom Line: You learn about debt through failure, not credentials.

How to Find $6,500 in Annual Savings

Over 1 million homeowners face rates double what they locked in during 2021.

First step? Track every dollar you spent monthly for the past year.

Find spending equal to your payment increase.

Separate expenses into categories.

Takeout. Subscriptions. Clothes. Groceries.

Most people guess 30% to 50% too low on these.

Split fixed costs (mortgage, car loans, insurance, property tax, utilities) from variable costs (groceries, gas, clothes, entertainment, travel, discretionary stuff).

Hit the high-impact reductions first.

Two large double-doubles from Tim Hortons daily? Almost $2,000 yearly.

Eating out or ordering in twice weekly costs Canadians $13,000 more per year versus cooking at home.

Double your mortgage increase right there.

New golf clubs or a leather coat? Redirect toward your mortgage.

Most homeowners find $6,500 through spending analysis.

The question isn’t affordability.

The question is whether you’ll trade today’s spending for tomorrow’s wealth.

Extending amortization means choosing comfort now over money later.

Bottom Line: The $13,000 dining premium covers double the mortgage increase. Cutting spending is a choice.

What Happens When Your Rate Bet Fails

Most homeowners are picking 3-year terms over 5-year terms right now.

They’re betting rates drop.

You’re gambling on something you can’t control.

Here’s what happens if you’re wrong.

Higher Payments: At renewal, your rate will probably be higher than before. Payments jump. Budgets get squeezed.

Payment Shock: The sudden jump makes managing other bills harder.

More Debt: Higher rates mean more of your payment goes to interest, not principal. Debt grows. Equity growth slows.

Qualification Problems: You’ll have trouble qualifying for a new mortgage if rates rose or your finances changed. Fewer options.

Forced Sales: Worst case? You can’t afford the new payment and need to sell, possibly at a loss if values dropped too.

No Room to Move: Locking in a high rate now with another high rate later? No wiggle room if things go sideways.

Bottom Line: The 3-year play is speculation. If you’re wrong, stress compounds across six ways.

How to Pay Down Your Mortgage Faster

Shopping rates and talking to brokers? Not enough.

They are table stakes.

Real wins come from payment structure and how you attack principal.

In 2026, winning on a 3-year term isn’t about the rate.

It’s about cutting your balance before your next renewal.

Drop your principal now. Lower starting balance in 2029 means lower stress at renewal.

Protection against payment shock.

Most homeowners miss three moves.

Move 1: The Extra Month from Accelerated Payments

Regular monthly or bi-weekly payments cover interest plus a bit of principal.

Switch to Accelerated Bi-Weekly or Accelerated Weekly? You make one extra monthly payment yearly.

How It Works: The extra payment goes 100% to principal. Skips interest completely.

The Result: On a typical 15-year mortgage, you’ll cut 2 to 3 years off.

Key Point: Changing payment timing cuts principal without needing extra cash.

Move 2: Lump Sum Prepayments

Most lenders let you prepay 10% to 20% yearly.

A 3-year term gives you three shots at this before your next renewal.

How It Works: Lump sums don’t change your monthly payment. They only cut your balance.

Why It Matters: When rates stay high, a lump sum gives you a guaranteed return equal to your rate (4.5% to 5%). Often beats savings accounts after tax.

Key Point: Lump sums deliver guaranteed, tax-free returns matching your mortgage rate. Better than most bonds in high-rate times.

Move 3: Payment Rounding

Shopping for rates is table stakes.

Manually bumping your payment? Missed opportunity.

Many 3-year deals let you increase payments 15% to 20% once yearly.

How It Works: If your 3-year rate is lower than current 5-year rates, pay at the higher rate. The gap goes straight to principal.

The Win: You stress test your budget for renewal while building equity faster.

Key Point: Payment rounding turns rate differences into principal cuts and budget practice.

How Much Cash to Keep Before Extra Payments

Before throwing lump sums at your mortgage in 2026, keep three to six months of living expenses liquid.

Covers job loss or big home repairs without forcing you into high-interest debt.

For homeowners, base this on these priorities.

Basic Reserve: 3 to 6 months covers essentials. Mortgage, utilities, property taxes, insurance, food, transportation.

Variable Thresholds:

Single Income: Aim for six months minimum. One job loss cuts all income.

Self-Employed or Irregular Pay: Go up to nine months.

Older Homes: Save past six months for surprise repairs.

Retirement: Keep way more if you’re retired or close to it. One to two years of expenses. Stops you from selling investments when markets tank.

Where to Keep It: Liquid accounts only. HISA or TFSA. Don’t put emergency money in stocks. They drop when you need cash most.

Quick check? $5,000 baseline.

Not a full cushion, but enough to cover a few $1,000 surprises before you lock money into mortgage payments.

Bottom Line: Match your reserve to your income stability and home age. Prepayment returns only work after you’ve built reserves.

Treat Your Mortgage Like Part of Your Portfolio

Data shows a pattern.

Homeowners who treat renewal as one-and-done? They lose.

Homeowners who treat it as ongoing rebalancing? They win.

Over a 15-year mortgage, ongoing rebalancing means comparing the guaranteed, tax-free return from paying down your mortgage against returns from stocks or bonds.

Active approach to managing your biggest debt alongside other assets.

In practice, mix calendar reviews with trigger points.

Regular Check-Ins

Twice yearly (every January and July), do these things.

Check Your Mix: View home equity like bonds or conservative assets. Look at your total mix (home equity and debt versus stocks, bonds, cash) against your risk comfort for your life stage.

Compare Returns: Stack your mortgage rate (your guaranteed return from prepayments) against after-tax returns from investments and rates on other debts.

Direct Your Money: Send new cash to wherever gives better risk-adjusted returns right now. High mortgage rates and weak markets? Pay the mortgage. Low mortgage rates and strong markets? Invest instead.

Key Point: Regular reviews turn your mortgage from a renewal event into continuous money management.

Trigger Point Adjustments

Make changes when your finances or markets shift past a threshold.

Rate Shifts: When rates move big, reassess. If rates drop, look at resetting parts of your mortgage early.

Life Changes: Revisit everything after job changes, inheritance, new kids, or nearing retirement. These shift your risk comfort and goals.

Equity Growth: As you build equity, your leverage drops. You might tap some through a HELOC to diversify if it fits your goals.

This approach skips emotional snap decisions. Makes informed adjustments to keep your full money picture aligned long-term.

Bottom Line: Ongoing rebalancing treats your mortgage as one piece of total assets, not isolated debt.

What Should 1.15 Million Canadian Homeowners Do Right Now?

For 1.15 million Canadian homeowners facing renewal in 2026, here’s the move.

Calculate your payment shock now.

Don’t wait for your lender’s 30-day notice.

Numbers for 2026 aren’t pretty. Most homeowners jump from pandemic rates below 2% to rates around 4.0% to 4.5%.

Average payment increases? 15% to 20%.

Around $500 to $700 monthly for typical mortgages.

Follow this plan for 2026.

Step 1: Run the Numbers

Use a mortgage calculator. Plug in 4.25%. Seeing the exact dollar increase turns fear into a budget item.

Step 2: Test Your Budget

Start putting aside the gap between current and projected 2026 payments into a HISA now. Builds a cushion and proves you’re ready.

Step 3: Use the 120-Day Rule

Call a broker four months before your renewal. Lock a rate hold. Sets a ceiling if rates spike, lets you benefit if they drop before you sign.

Step 4: Use New Switch Rules

2024 rule changes let you switch lenders without requalifying under stress tests for straight switches (no increase, no extension). Way more negotiating power.

Step 5: Know Your Safety Valve

If the new payment won’t work, talk to a broker about extending to 25 years. Costs more interest long-term but cuts hundreds monthly short-term.

The $100,000 gap wipes out equity growth.

Kills investment gains.

Transfers wealth from you to lenders.

Bottom Line: Calculating shock four months early turns crisis into solvable problem with options.

Your Questions Answered

How much extra will I pay if I extend my mortgage from 15 to 25 years?

On a $400,000 mortgage at 4%, extending from 15 to 25 years cuts monthly payments by $850. Total interest jumps from $132,000 over 15 years to $233,000 over 25 years. Extra $100,000+ in interest.

Should I auto-renew with my lender?

No. 69% of Canadians auto-renew and pay $155 more monthly versus those who shop around. Over five years, $9,300 wasted. Shopping around isn’t optional.

What’s the return on a lump-sum prepayment?

Guaranteed return equals your mortgage rate. At 4.5% to 5%, often beats savings accounts after tax.

How much emergency cash should I keep before extra payments?

Keep three to six months of living expenses liquid before lump sums. Single income? Aim for six months minimum. Self-employed? Up to nine months.

Is a 3-year term better than 5-year in 2026?

A 3-year term bets rates drop. If you’re wrong and rates stay up or climb, you’ll face higher payments, shock, more debt, qualification issues, possible forced sale, and less flexibility at renewal.

What are the three moves most homeowners miss?

Three moves: accelerated bi-weekly or weekly payments (adds one extra monthly payment yearly), lump-sum prepayments (10% to 20% yearly), and payment rounding (boosting regular payments 15% to 20% once yearly).

How do I find $6,500 yearly to cover payment increases?

Check spending by category. Canadians spend $13,000 more yearly eating out versus cooking at home. Two large Tim Hortons daily? Almost $2,000 yearly. Split fixed from variable costs and hit big cuts first.

What’s the 120-Day Rule?

Call a broker four months before renewal to lock a rate hold. Sets a ceiling if rates spike, lets you benefit if they drop before signing.

What You Need to Remember

-

Extending from 15 to 25 years costs an extra $100,000+ in interest for only $850 monthly relief. Wipes out equity growth and transfers wealth to lenders.

-

Auto-renewing costs $9,300 over five years. Shopping around and negotiating aren’t optional. They’re basic moves for renewal.

-

Three acceleration moves: faster payment timing, lump sums (guaranteed returns matching your rate), and payment bumps. These cut 2 to 3 years off amortization and save tens of thousands in interest.

-

Build reserves before prepayments. Keep three to six months of expenses liquid. Single income and self-employed need bigger cushions.

-

Treat renewal as ongoing rebalancing, not one-time event. Review twice yearly and adjust when rates shift, life changes, or equity grows.

-

3-year terms bet on rate drops. If wrong, you face payment shock, more debt, qualification trouble, possible forced sale, and less flexibility.

-

2026 plan: calculate shock four months early, test your budget, lock rate holds via 120-Day Rule, use new switch rules, know your safety valve before deadlines.

Go run your numbers now.